Partial autocorrelation function (PACF) can be defined as a time series where there is a restricted or incomplete correlation between the values for shorter time lags.

PACF is not at all like ACF; with PACE the autocorrelation of a data point at the current point and the autocorrelation at a period lag have a direct or indirect correlation. PACF concepts are heavily used in autoregressive models.

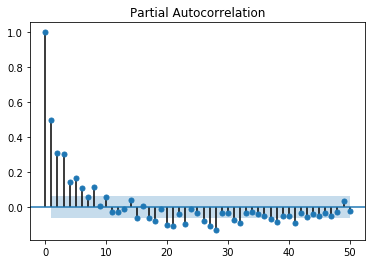

In Python, the PACF function can be computed as follows:

import matplotlib.pyplot as plt

import numpy as np

import pandas as p

from statsmodels.graphics.tsaplots import plot_pacf

data = p.Series(0.7 * np.random.rand(1000) + 0.3 * np.sin(np.linspace(-9 * np.pi, 9 * np.pi, num=1000)))

plot_pacf(data, lag = 50)

pyplot.show()

The output for PACF can be seen as shown: